Published: · Reviewed by Ertuğrul Öz, Certified Fire Chief & Training Specialist

Homeowners insurance after a fire does not work the way most people expect. The policy that felt straightforward when you bought it — "if my house burns down, they pay to rebuild it" — turns out to have four separate coverage components, multiple valuation methods, depreciation calculations, exclusions that apply in specific scenarios, and a claims process that rewards the organized and penalizes those who are not. Most homeowners discover the details of their policy for the first time while standing in front of a burned house.

This is what the policy actually covers, how the numbers are calculated, what it does not cover that surprises people most, and how to navigate the claims process without leaving money on the table that you are entitled to.

In this article:

- The four coverage components of a homeowners policy

- Replacement cost vs. actual cash value: the most important distinction

- Dwelling coverage: why most homes are underinsured

- Personal property: how depreciation works in practice

- Additional living expenses: what it covers and for how long

- What homeowners insurance does not cover after a fire

- The claims process in detail

- Public adjusters: what they do and when to use one

- The home inventory and why it matters more than people think

The Four Coverage Components of a Homeowners Policy

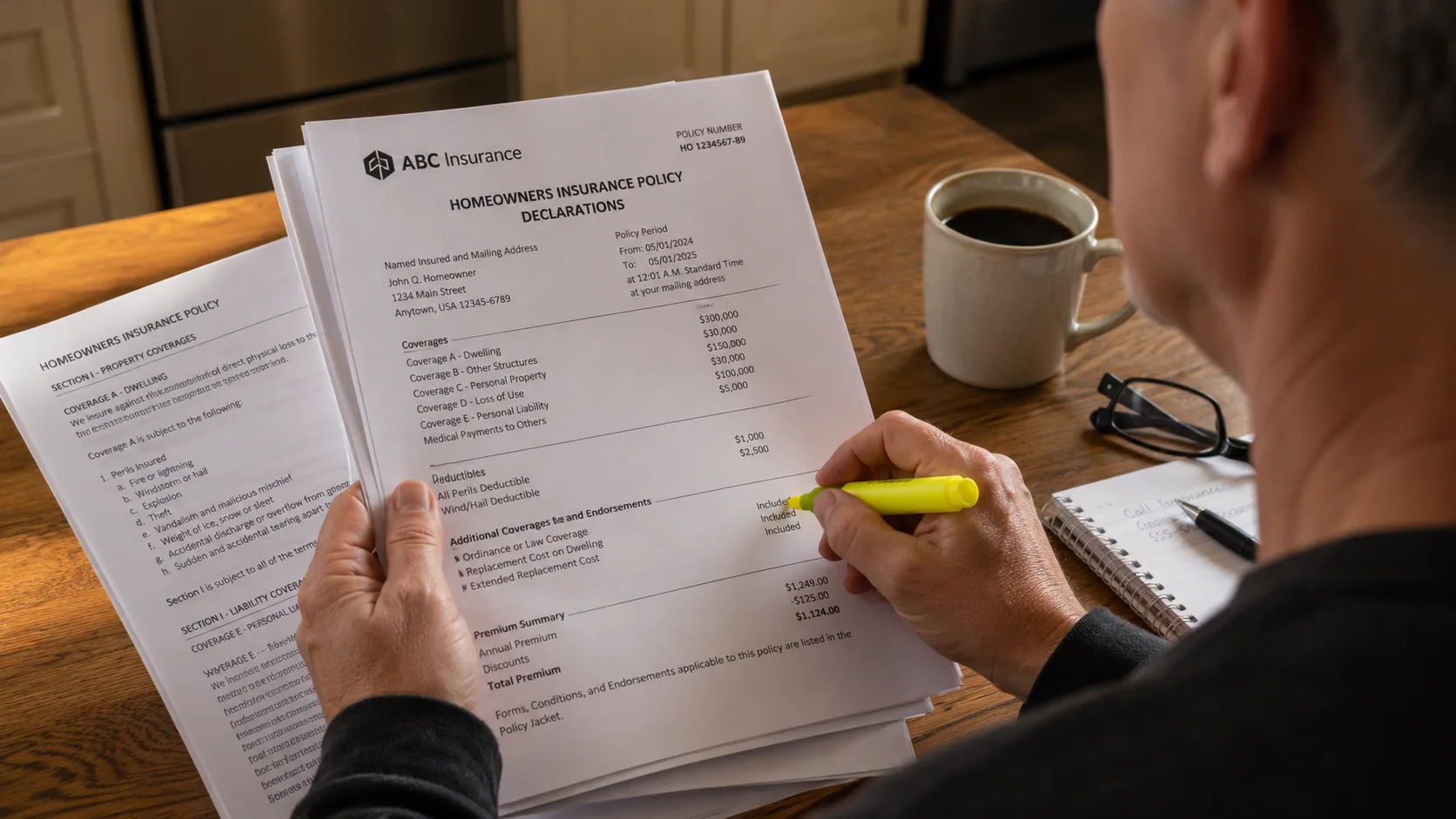

A standard homeowners insurance policy (HO-3 is the most common form) has four major coverage sections. Understanding them separately is the foundation for understanding the claim.

Coverage A — Dwelling

Pays to repair or rebuild the physical structure of your home — the walls, roof, foundation, built-in appliances, and attached structures. This is the number that appears on your declarations page as your coverage limit. Whether that limit is sufficient to actually rebuild your home is a separate question covered below.

Coverage B — Other Structures

Covers detached structures on the property — a detached garage, a fence, a shed. Typically set at 10 percent of the Coverage A limit by default, adjustable upward.

Coverage C — Personal Property

Covers the contents of your home — furniture, clothing, electronics, appliances. Typically 50 to 70 percent of the Coverage A limit, though this is adjustable. Personal property coverage has its own valuation method (replacement cost or actual cash value) and specific sub-limits for categories like jewelry, art, and firearms that may be far below what you own.

Coverage D — Additional Living Expenses

Pays the increased cost of living while your home is uninhabitable — hotel, rental housing, restaurant meals above your normal food budget, laundry, storage. Typically 20 to 30 percent of Coverage A, with a time limit of 12 to 24 months depending on the policy.

Replacement Cost vs. Actual Cash Value: The Most Important Distinction

This distinction applies to both dwelling coverage and personal property coverage, and it is the single most financially significant detail in a homeowners policy.

Replacement Cost Value (RCV)

Pays what it costs to replace the item or rebuild the structure with equivalent new materials at current prices, without deducting for age or condition. A five-year-old refrigerator that cost $800 is replaced with a comparable new refrigerator at whatever it currently costs — say $950. The policy pays $950. This is the better coverage and costs more in premium.

Actual Cash Value (ACV)

Pays replacement cost minus depreciation — an adjustment for the age and condition of the item. The same five-year-old refrigerator is assessed at its current market value given its age and condition. The adjuster may determine that $800 refrigerator, five years old, is worth $350 today. The policy pays $350. You replace a $950 refrigerator with $350 — and pay the $600 difference yourself.

The ACV method applied across an entire house full of contents — furniture, appliances, electronics, clothing, all of it at varying stages of age and depreciation — can result in a personal property payout that covers a fraction of what replacement actually costs. Many policyholders with ACV coverage discover this only after the fire, when the settlement is delivered and they realize they cannot replace their contents at the compensation level provided.

Check your policy now: look for "replacement cost" or "actual cash value" in the personal property section. If it says ACV and you have significant personal property, the upgrade to RCV is typically $50 to $150 per year in additional premium — almost certainly worth it.

Dwelling Coverage: Why Most Homes Are Underinsured

An estimated 65 percent of insured homes in the U.S. are underinsured — their Coverage A limit is insufficient to fully rebuild the home at current construction costs. The gap averages around $40,000 but can be far higher in markets where construction costs have risen rapidly. This is not because homeowners are careless. It is because construction costs change, home values change, and most homeowners set their coverage limit once and do not revisit it.

The market value of your home and the cost to rebuild it are different numbers. Market value includes the land, which does not burn. It reflects supply, demand, neighborhood, and location. Rebuild cost reflects current labor rates, material prices, and the cost of clearing debris and meeting current building codes. In many markets, rebuild cost per square foot has increased 30 to 50 percent in the past five years. A Coverage A limit set five years ago based on a rebuild cost estimate may now cover only 60 to 70 percent of actual rebuild cost.

Extended and guaranteed replacement cost endorsements

Extended replacement cost endorsements add a buffer — typically 25 to 50 percent above the Coverage A limit — to account for unexpected cost overruns. If your limit is $400,000 and rebuilding costs $500,000, a 25 percent extended replacement cost endorsement covers $500,000. Guaranteed replacement cost endorsements, available from some insurers, cover the full rebuild regardless of cost — the most comprehensive protection but also the most expensive and not universally available.

If you have neither endorsement and your Coverage A limit does not cover full rebuild cost, you pay the difference out of pocket or accept a partial rebuild. Review your coverage limit annually and cross-check it against local construction cost estimates — your insurer may provide an online calculator, or a local contractor can give you a rough per-square-foot rebuild estimate.

Personal Property: How Depreciation Works in Practice

Even with replacement cost coverage on personal property, the initial payment from the insurer is typically the actual cash value. The RCV payout process works in two steps: the insurer pays ACV first, and then pays the remaining RCV amount — called the "recoverable depreciation" — after you demonstrate that you have actually purchased the replacement item. You have to spend the money to recover the depreciation.

This is a cash flow issue that many fire survivors do not anticipate. After a major fire, you may receive an initial personal property payment that covers some but not all of your immediate replacement needs. To recover the full replacement cost, you must buy the replacement and submit the receipt. If you cannot afford to buy the item before receiving the depreciation recovery, you are in a gap period. Knowing this process in advance helps you prioritize which replacement purchases to make first to recover the most depreciation.

Sub-limits on specific categories

Standard homeowners policies contain specific sub-limits for categories of personal property, regardless of the overall personal property coverage limit. Common sub-limits in HO-3 policies include: jewelry ($1,000 to $1,500 per item, $2,500 aggregate), firearms ($2,500), silverware ($2,500), cash ($200), business property in the home ($2,500), and fine art or collectibles (limited or excluded). If you own items that fall into these categories and their value exceeds the sub-limits, you need a scheduled personal property endorsement — a specific rider that lists and covers those items at their appraised value. Without it, a $15,000 engagement ring is covered at $1,500.

Additional Living Expenses: What It Covers and for How Long

ALE coverage pays the difference between what you are spending on temporary housing and meals and what you normally spend. It does not pay your full hotel bill — it pays the amount above what you would have spent living at home. If your normal monthly housing cost is $2,000 and your temporary rental is $3,500, ALE covers $1,500 per month, not $3,500.

ALE has two limits: a dollar limit (typically 20 to 30 percent of Coverage A) and a time limit (typically 12 to 24 months). If your home takes 18 months to rebuild and your policy has a 12-month time limit, the last six months of temporary housing are your expense. If construction costs or contractor delays push the rebuild past your time limit, you absorb those additional living costs.

Document every ALE expense — hotel receipts, restaurant receipts, storage unit costs, additional commuting costs, pet boarding (usually covered), laundry costs above normal. Insurers pay ALE based on submitted documentation. Undocumented expenses are not reimbursed.

What Homeowners Insurance Does Not Cover After a Fire

| Scenario | Covered? | Notes |

|---|---|---|

| Fire caused by negligence (leaving stove on, candle unattended) | ✓ Yes | Negligence is covered — intentional acts are not |

| Arson committed by the policyholder | ✗ No | Intentional damage by the insured voids coverage; also a felony |

| Fire in a vacant home (30–60 days unoccupied) | ✗ No | Most policies exclude fire in structures vacant beyond the policy's vacancy clause — typically 30 or 60 days |

| Water damage from firefighting | ✓ Yes | Covered under dwelling and personal property as a direct result of the fire event |

| Mold from firefighting water (if addressed promptly) | ✓ Usually | Mold from fire water is typically covered as consequential damage if remediated promptly; mold from pre-existing conditions is not |

| Earthquake-caused fire | Varies | Fire following earthquake is typically covered; the earthquake damage itself usually requires a separate earthquake policy |

| Vehicles in a garage | ✗ Not under homeowners | Vehicles are covered under comprehensive auto insurance, not homeowners — even if destroyed in a house fire |

| Business inventory or equipment in the home | Partial | Sub-limited under HO-3; home business endorsement required for significant business property coverage |

| Code upgrade costs | Partial | Standard policies pay to rebuild to pre-fire condition; if local codes require upgrades (updated electrical, fire suppression), a code upgrade endorsement covers that additional cost |

The Claims Process in Detail

The claims process after a major fire typically runs in three parallel tracks: the dwelling claim (rebuilding the structure), the personal property claim (replacing contents), and the ALE claim (temporary housing reimbursement). All three run simultaneously, all three involve documentation, and all three may involve negotiation.

The insurer assigns an adjuster — either a staff adjuster employed by the company or an independent adjuster contracted for the claim. The adjuster's job is to assess covered damages and apply the policy terms to calculate the settlement. They are not adversaries, but they are also not your advocate — their assessment reflects the insurer's position, not necessarily your full entitlement under the policy.

The dwelling settlement process: the adjuster prepares an estimate of repair or replacement cost using a standard estimating program (Xactimate is the most common in the industry). The estimate is provided to you. You have the right to obtain your own contractor estimates and to dispute the adjuster's numbers if your estimates differ materially. Many settlements are resolved through negotiation between the adjuster's estimate and contractor bids.

The personal property settlement process: you submit an itemized list of all contents lost or damaged, with descriptions, purchase dates where known, and values. The adjuster reviews the list, applies depreciation (if ACV) or values at replacement cost (if RCV), and issues a settlement. Items you cannot document may be challenged or reduced. Items you forgot to list cannot be added after the settlement is accepted.

Public Adjusters: What They Do and When to Use One

A public adjuster is a licensed professional who represents the policyholder — not the insurer — in the claims process. They review your policy, document damages, prepare and submit the claim, and negotiate with the insurer on your behalf. They are paid a percentage of the final settlement, typically 5 to 15 percent.

Public adjusters add value in specific situations: large or complex claims where the dwelling estimate involves significant items (custom finishes, unusual construction, code upgrades); claims where the insurer's initial settlement seems significantly below what the damage warrants; and cases where the policyholder lacks the time or expertise to document and negotiate a comprehensive claim. They do not add value in straightforward small claims where the insurer's assessment is accurate and uncontested — their fee comes out of your settlement, so they need to recover more than their fee to be worth engaging.

If you consider a public adjuster, verify their license with your state insurance commissioner, check references from previous fire claims, and confirm the fee structure in writing before signing anything. Public adjuster fraud — unlicensed practitioners targeting fire survivors — exists alongside contractor fraud and is addressed by the same state insurance commissioner's office.

The Home Inventory and Why It Matters More Than People Think

The personal property claim requires you to list everything you lost. After a fire that destroys the contents of a 2,000-square-foot home, "everything you lost" is thousands of items — every piece of clothing, every kitchen utensil, every book, every piece of electronics, every tool. Most people cannot reconstruct that list accurately from memory weeks after the event, in the middle of a crisis.

A home inventory — a documented record of your possessions, ideally with photographs and purchase receipts — is the preparation that makes a personal property claim substantially more complete and therefore substantially more fully compensated. It does not need to be elaborate. A walkthrough of your home with your phone's video camera, narrating what you see in each room and opening drawers and closets, creates a record that is infinitely more useful than memory alone.

- ✓Video walkthrough of every room — open closets, drawers, cabinets. Narrate brand names and approximate quantities where visible.

- ✓Photograph serial numbers on appliances and major electronics — makes identification and valuation faster.

- ✓Store the inventory off-site or in the cloud — a video stored only on a home computer or a local hard drive is destroyed in the same fire it was meant to document.

- ✓Update annually — major purchases added to the home should be added to the inventory when bought, not reconstructed from memory later.

- ✓Keep purchase receipts for major items — store digital copies in the cloud or with your insurance documents.

- ✓Get appraisals for high-value items — jewelry, art, collectibles, musical instruments — and add a scheduled personal property endorsement for anything that exceeds standard sub-limits.

The gap between what a documented claim recovers and what an undocumented claim recovers — across every category of personal property — is real and consistently significant. An afternoon creating a home inventory and storing it off-site is insurance for your insurance.

Comments 0

No comments yet. Be the first to share your thoughts!

Leave a Comment